Finding the Best Medical Credit Card Braces: Your 2025 Guide to Affordable Orthodontic Care

Did you realize that there are almost 4 million Americans wearing braces with a quarter of them being adults? Orthodontic is now even more popular than ever and the cost may become a serious obstacle. Having a mean price of between 3,000 and 7,000 dollars per braces or more in the case of complicated cases, most patients ask: How can I afford that without tapping my savings?

This all-inclusive manual will help to demystify the procedure of utilizing medical credit cards in order to cover orthodontic treatment. We will discuss the most suitable medical credit card to use when getting braces, we will evaluate your options of financing, and we will unlock secret tips to ensure your process of getting yourself a flawless smile is not only cheap but also easy.

Understanding Medical Credit Cards: How They Work for Orthodontic Care

Medical credit cards are the specialized financial products that are aimed at healthcare costs. They are usually provided with promotional financing conditions unlike the traditional credit cards making it easier to obtain the braces in case of medical card financing.

How Medical Credit Cards Differ from Regular Credit Cards

- Purpose-Limited: Can only be used at participating healthcare providers

- Promotional Periods: Often feature 0% interest for 6-24 months

- Provider-Specific: Acceptance varies by dental practice

- Quick Approval: Decisions often within minutes

The Pros and Cons of Using Medical Credit for Braces

Advantages ✓

- Interest-free promotional periods

- Predictable monthly payments

- Immediate treatment access

- Potentially higher approval rates

Considerations ⚠️

- Deferred interest risks

- Limited to participating providers

- Potential impact on credit score

- Higher rates after promotional period

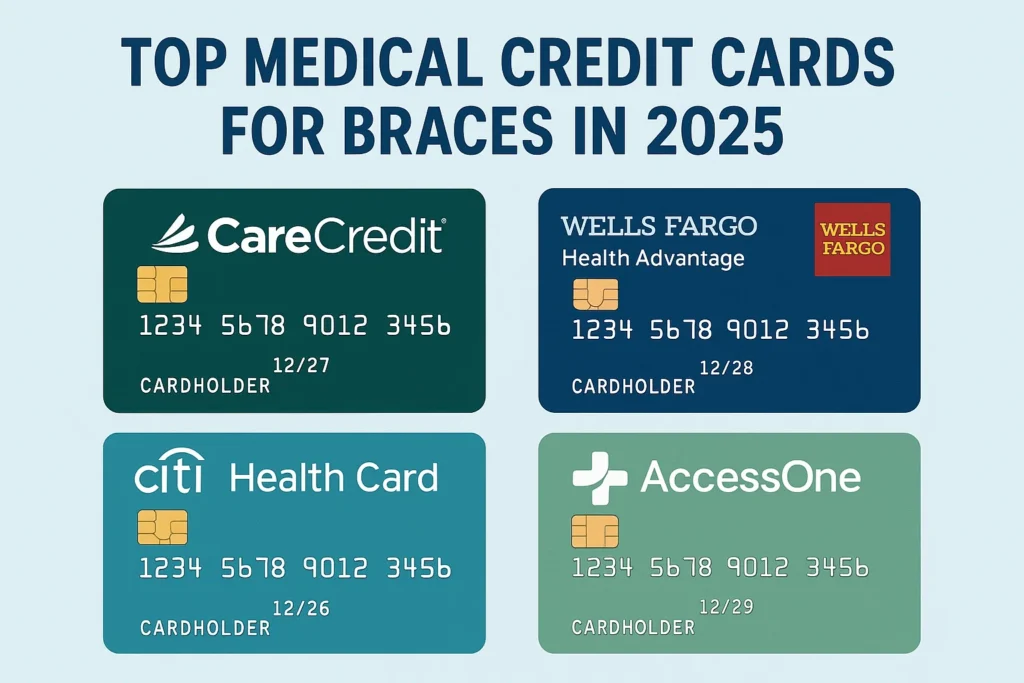

Top Medical Credit Cards for Braces in 2025

After extensive research and analysis of current market offerings, here are the leading options for medical aid for braces through credit financing.

1. CareCredit: The Industry Leader

CareCredit for braces remains the most widely accepted medical credit card nationwide, accepted by over 250,000 healthcare providers.

Key Features:

- Promotional periods: 6, 12, 18, or 24 months interest-free

- Minimum purchase: $200 for promotional financing

- Widest acceptance among orthodontists

- Can be used for follow-up appointments and adjustments

Best for: Patients seeking the most flexible and widely accepted option.

2. Alphaeon Credit: Specialized for Elective Procedures

Alphaeon focuses specifically on elective healthcare, making it ideal for orthodontic treatment.

Key Features:

- Long-term financing: Up to 60 months available

- No annual fee

- Online account management

- Special offers throughout the year

Best for: Patients needing longer repayment terms for extensive treatment.

Comparison Table: Medical Credit Cards for Braces

| Feature | CareCredit | Alphaeon Credit | Citi Health Card |

|---|---|---|---|

| Interest-Free Period | 6-24 months | 12-60 months | 6-18 months |

| Provider Network | 250,000+ | 10,000+ | 50,000+ |

| Minimum Purchase | $200 | $399 | $500 |

| Credit Check | Yes | Yes | Yes |

| Best For | Maximum flexibility | Long-term financing | Established credit users |

Alternative Financing Options for Braces

While medical credit cards are popular, they’re not your only option for affordable braces without credit check concerns or traditional financing.

In-Office Payment Plans

Many orthodontists offer direct payment plans that don’t involve third-party financing.

Benefits:

- No credit check required

- Customized to your budget

- Often interest-free

- Simplified billing

Pro Tip: Always ask about in-office plans before exploring external financing. Many top dentists offering help with braces provide this option.

Dental Discount Plans

These are membership programs that provide discounted rates on dental services, including orthodontics.

How they work:

- Annual membership fee ($100-200)

- 15-50% discount on treatment costs

- Pay discounted amount upfront or through payment plan

- No waiting periods typically

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

If you have access to these tax-advantaged accounts, they can significantly reduce your out-of-pocket costs for braces.

Key advantages:

- Pre-tax dollars reduce effective cost by 20-30%

- Can be combined with other financing methods

- No credit impact

How to Choose the Right Financing Option for Your Braces

Selecting the best financing approach requires careful consideration of your financial situation and treatment needs.

5-Step Decision Framework

- Get a Detailed Treatment Quote: Understand the total braces price with medical aid or without.

- Assess Your Credit Health: Check your credit score before applying.

- Compare All Available Options: Don’t settle for the first offer.

- Calculate the True Total Cost: Include interest if promotional periods expire.

- Read the Fine Print: Understand deferred interest terms completely.

Warning: The Deferred Interest Trap

⚠️ Important: Many medical credit cards use deferred interest. If you don’t pay the entire balance within the promotional period, you’ll owe interest from the original purchase date. Always have a repayment plan!

Finding the Right Orthodontic Provider

Your financing options are often tied to the provider you choose. Here’s how to find braces near me with monthly payments from reputable practices.

What to Look for in an Orthodontic Practice

- Transparent pricing and financing discussions

- Multiple payment options

- Positive patient reviews

- Board-certified orthodontists

- Complimentary consultations

Questions to Ask During Your Consultation

- “What financing options do you offer?”

- “Do you work with patients to create affordable payment plans?”

- “Are there any hidden fees in the treatment cost?”

- “What happens if I experience financial difficulty during treatment?”

Frequently Asked Questions About Medical Credit Cards for Braces

Q: Can I get braces with no credit check?

A: Yes, via in-office payment programs provided by particular orthodontists. These plans do not usually include credit checks but they might need a down payment.

Q: What is my credit score to take CareCredit?

A: CareCredit usually needs a fair to good credit score (usually 620 and above), although it depends on various factors such as income and debt to income ratio.

Q: Does it include braces in the medical assistance of adults?

A: The orthodontic coverage of adult patients is limited or absent in most medical aids (health insurance). Children below 18 are more covered. Never count on your particular plan.

Q: What is going to happen when I am unable to make payments in the course of treatment?

A: Get in touch with your provider. A lot of orthodontists will also deal with patients who are poor and they will make arrangements to revise the payment plans instead of discontinuing the treatment.

Q: Does medical credit card have income requirements?

A: Yes, issuers look at your earnings about your already existing debts. No particular minimum is needed, and one must have enough money to pay.

Q: Does the number of ways of braces financing depend?

A: Absolutely. HSA/FSA funds are often used together with a medical credit card or plan of payment to finance less.

Conclusion: Your Path to an Affordable Beautiful Smile

Finding the funds to finance braces is not as daunting. The most appropriate medical credit card to use in braces is that which matches with your budget and dental care schedule. It either gets CareCredit, a payment plan in the office or a combination of both strategies, but the point is to study extensively and know all terms.

Ready to take the next step? Begin by making appointments with the best dentists who provide services with braces in your locality. Talk about the methods of financing your practice at your appointment, and feel free to ask specific questions. The right financial strategy will help you to have your ideal smile.

Best Toothbrush Braces Cleaning: Top Picks for a Perfect Smile